Why quality stocks perform so well

In the smart beta world, companies with high profitability are often called ‘quality stocks’ as opposed to ‘junk stocks’ that are loss-making or have low profitability. Robert Novy-Marx was probably the first to describe this profitability premium and bring it to the attention of a wider audience. While the quality factor is not necessarily universally accepted, I recently discussed how it is one of five factors that allow you to cover the entire factor zoo.

Anwer Ahmed, Michael Neel, and Irfan Safdar wanted to know why companies with higher profitability systematically outperform those with lower profitability. After all, if markets were efficient, higher profitability should be reflected in higher starting valuations and future returns of highly profitable companies should be no different from the returns of less profitable ones.

But that is clearly not the case, so the question is if the outperformance of highly profitable companies reflects higher risks or systematic market mispricing.

It could be that companies with higher profitability have higher risks because with higher profitability comes the potential for future disappointments and corresponding share price drops. However, their analysis showed that companies with higher profitability have a lower probability of future share price crashes (rather than a higher probability). Similarly, in extremely negative months, shares of companies with higher profitability tend to outperform the shares of companies with lower profitability. Again, this is not what one would expect if the profitability premium were compensation for higher risk. Indeed, companies with higher profitability have on average lower risk.

If the profitability premium is not a compensation for risk, maybe it is simply a reflection of systematic mispricing in markets. This seems to be what is going on. In the study, they looked at analyst estimates of future corporate profits and revisions of these estimates.

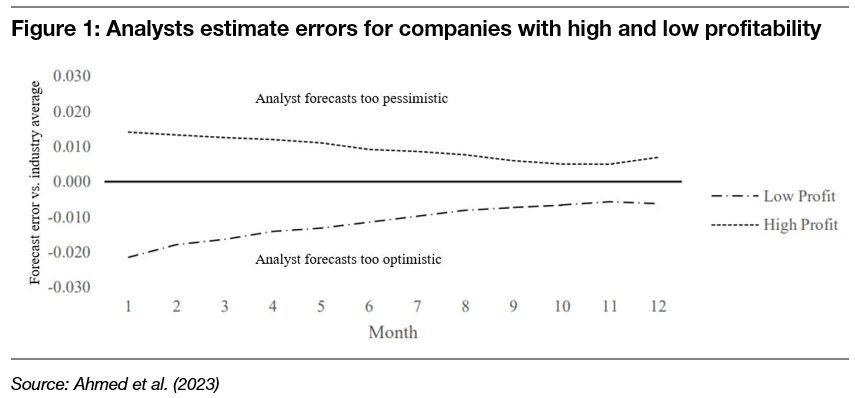

The chart to the left shows what happens on average to the 10% most and least profitable businesses in the US. On the horizontal axis, you see the months of a financial year, and on the vertical axis the estimation error relative to the average estimation error for companies in the same industry. Weirdly, the authors decided to plot the chart in such a way that analysts overestimating future profitability have a negative estimation error and analysts underestimating future profits have a positive error. Hence, the chart below shows that for companies with high profitability, analysts tend to underestimate future profitability but then revise their estimates upward over the financial year. For companies with low profitability, analysts overestimate future profitability and then need to revise their estimates lower as the year progresses.

The result is that these earnings revisions drive the share price of highly profitable companies higher during the year and the shares of low profitability companies lower. And this is good news for investors because it means that investing in highly profitable companies is not associated with higher risks, and at the same time based on behavioural biases that are unlikely to change over time, so the effect should be relatively persistent.

Thought of the Day features investment-related and economics-related musings that don’t necessarily have anything to do with current markets. They are designed to take a step back and think about the world a little bit differently. Feel free to share these thoughts with your colleagues whenever you find them interesting. If you have colleagues who would like to receive this publication please ask them to send an email to joachim.klement@liberum.com. This publication is free for everyone.